Quarter in review

Global equities navigated a more complicated path in the September quarter but still ended at all-time highs. Early August saw sharp volatility due to weaker U.S. labour data, a Bank of Japan interest rate hike, and thinner market liquidity. However, joining other developed market central banks, the Federal Reserve’s long-anticipated rate-cutting cycle began in September, supporting a rally in stocks towards the quarter’s end and increasing hopes of the U.S. economy achieving a soft landing. The Fed’s decision came after holding rates steady for over a year, gaining greater confidence that inflation was moving sustainably towards 2%.

Policy rate easing was further priced into markets, boosting fixed income markets. Despite some volatility, credit spreads remained tight and global high-yield and corporate credit continued to outperform within fixed income. Global value equities outperformed growth stocks, with more interest-sensitive sectors such as global utilities, REITs and small caps outperforming, buoyed by hopes of the U.S. economy soft landing and lower interest rates, while U.S. mega-cap tech slowed down. Australian equities strengthened close to 8% during the quarter, with all sectors except utilities and energy advancing, and mid-cap and information technology sectors leading.

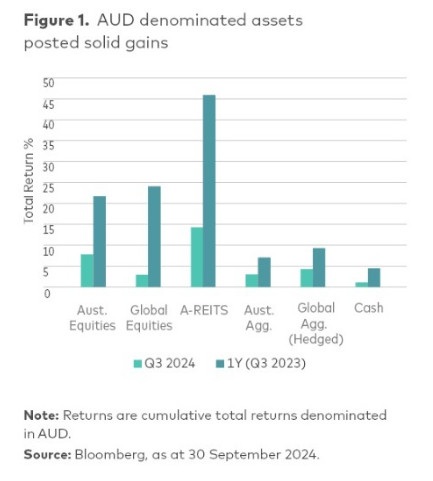

Australian REITs outperformed the broader Australian equity market, up over 45% for the year (Figure 1), benefiting from strong performances by the highest-weighted members in the concentrated REIT index.

Emerging markets experienced a last-minute boost from China’s accommodative stimulus measures, which included reduced mortgage rates and relaxed home-buying restrictions in major cities. This drove a significant surge in the local equity market (Figure 2).

Economic outlook

14 months after its last rate hike in July 2023, the Fed officially entered an easing cycle, implementing a larger-than-expected 50 basis point rate cut. This move comes just days before China announced a series of monetary, property, and market support measures, hinting that additional fiscal stimulus is likely on the horizon. With the Fed and other major economies taking steps toward policy easing, other emerging markets central banks now have an opportunity to follow suit.

The U.S. economy is moderating from its elevated pace in 2023, however growth still remains healthy in a range around trend, currently around 2.3% through the September quarter.

In Europe, however, there is little room for cheer. Manufacturing continues to struggle, pinned back by the lingering effects of the energy crisis and a slowdown in Chinese growth. Meanwhile, services activity is moderating amid restrictive monetary and fiscal policy, while floods in central and Eastern Europe will darken the growth outlook further.

In China, growth momentum has been fading in recent months, reflected in the miss in June quarter GDP, softer consumption momentum, and the still weak property sector. That said, policymakers have reiterated their goal to reach this year’s 5% growth target.

A recent policy ramp-up should lead to additional fiscal and monetary support and help move growth back on track, although there are still downside risks for the economy.

In Australia, inflation remains high despite weakening growth momentum. In the June quarter, GDP growth slowed to 0.2% quarter-on-quarter (in seasonally adjusted terms), the weakest pace outside the pandemic since the early 1990s recession, largely due to the Reserve Bank of Australia’s (RBA) monetary policy tightening. The persistence of inflation pressures in Australia is partly due to supply-side constraints, keeping the economy near full capacity despite softening demand.

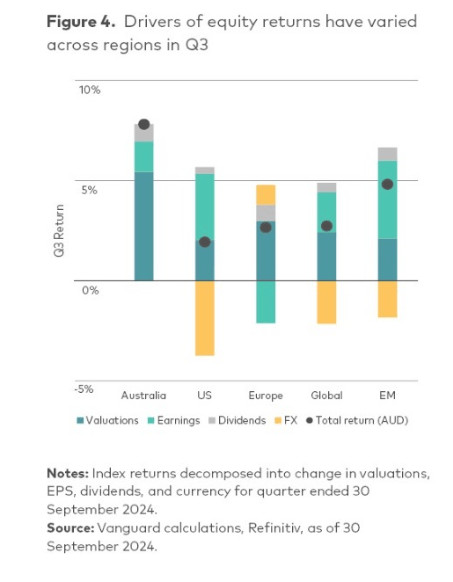

As central banks increasingly move to cut rates, markets have remained focused on the path forward for economies. Over the past year, investors have looked through weakness in earnings, but divergence in economic pace across regions continues to pose questions for markets. Indeed, breaking down the past quarter’s performance (Figure 4), U.S. earnings have again shown relative strength, in contrast to weakness in Europe and an expected rebound in Australia.

In bond markets, yields remain relatively attractive even as global central banks turn to rate cuts. Higher neutral rates are expected to support bond yields through the cycle and hence fixed income returns. Although long-term yields in some markets remain comparable to cash rates in markets like Australia, bonds allow investors to lock in these rates over longer time horizons as shorter-term rates fall, with coupons expected to provide more of a buffer against price movements compared with the post-GFC era.