Quarter in review

Global equities reached record highs by quarter end despite a hawkish view from investors on interest rates as inflation cooled slower than expected. This equity strength was driven by still-resilient economic data that continued

to support the prospect of a ‘soft landing’. However, the shift higher in yields over the quarter hampered fixed income assets, with the Bloomberg Global Aggregate Index (AUD Hedged) posting a -0.3% return. Australian yields, however, were broadly lower over the quarter, lifting Australian bond returns to 1.0%, with the Reserve Bank of Australia (RBA) also softening its hawkish forward guidance in its March meeting.

For Australian denominated assets, REITs outperformed, followed by global equities (Figure 1).

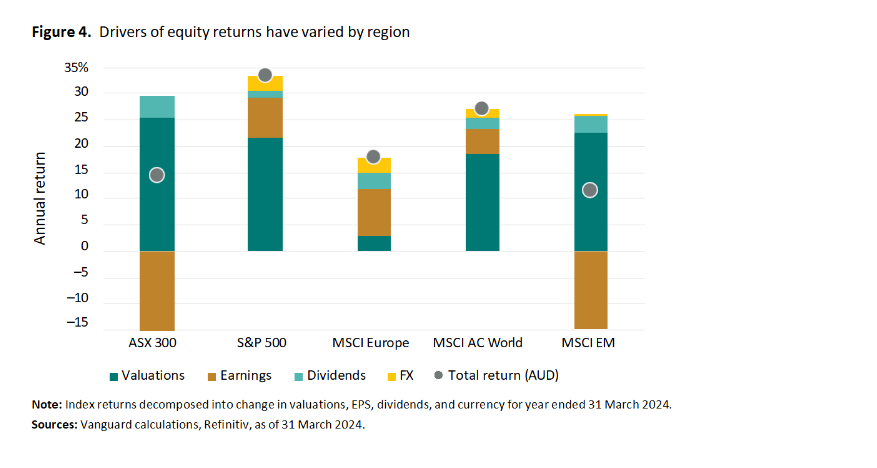

Global growth stocks outperformed, led by technology as AI boom sentiment continued to intensify. Japanese equities outperformed despite the Bank of Japan announcing an end to its negative interest rate policy and yield curve control. Australian equities advanced 5.4% but lagged peers, with the materials sector detracting while small caps outperformed. Chinese equities rebounded 1.2% over the quarter from better economic data and some policy easing from the People’s Bank of China (Figure 2).

Commodity prices were broadly higher in March, led by precious metals and energy, while agricultural products were broadly weaker. The U.S. dollar started to appreciate again as a less aggressive cutting cycle from the U.S. Federal Reserve (Fed) was discounted by markets.

Economic and market outlook

Despite inflation cooling among most major developed economies and providing some comfort to central banks, there are clear regional differences. The U.S. exceptionalism hasn’t shown any meaningful signs of fading out, with growth still above the pre-COVID trend and boosted further by supply side forces. The Australian economy has proven broadly resilient, with signs of recovering consumer sentiment, business confidence significantly improving this year, and the government running a modest fiscal deficit to fund investment in certain key sectors.

The story elsewhere has been very different, with tentative signs that economic momentum in Europe bottomed in Q4 2023 and may remain below trend in 2024 amid still restrictive monetary and fiscal policy, and the lingering effects of the energy crisis. The Chinese economy is still challenged by persistent headwinds, including a prolonged property downturn, subdued business confidence, with the output gap expected to close by end-2025, while inflation is likely to remain subdued given the widening supply-demand imbalance.

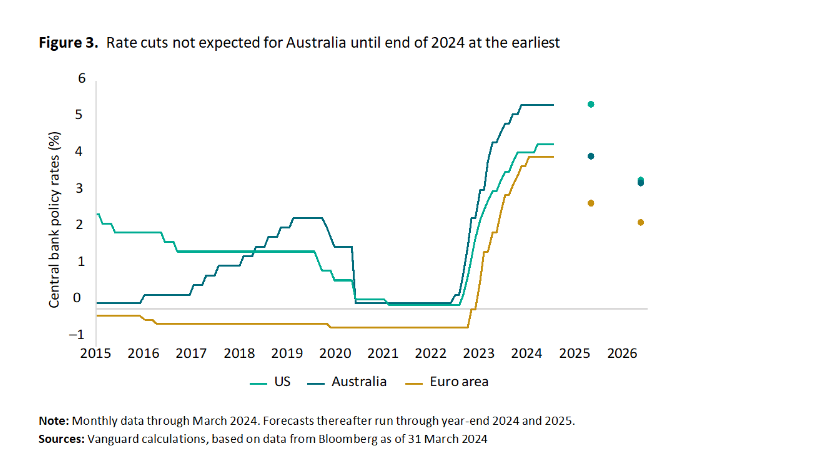

Australia has seen growth moderating, as intended by the RBA’s cash rate policy. Still, domestic and wage-driven inflation are poised to remain elevated, buoyed by incremental increases in real household income, resurgence in the housing market, and sustained investments in key sectors such as education, healthcare, and transportation, facilitated by a modest fiscal deficit.

The inflation call also rests on the developments in the housing and labour markets. Although the unemployment rate has ticked up of late, strong wage growth and slow productivity gains have led to a slower disinflation process than expected. As productivity growth has lagged, unit labour costs are outpacing levels consistent with the RBA’s 2–3% inflation target, reflecting some of the ‘sticky’ components of inflation. Moreover, inward migration has added to housing demand, feeding into sticky price pressures via higher rents. The labour market also remains at historically tight levels, with the employment- to-population ratio close to a multi-decade high, so the path to eventual policy easing could be longer.

Looking forward, broad pressures may persist, but earnings growth abroad should remain a larger driver of returns for international equities than for the local Australian market. Meanwhile, markets also looked towards interest rate cuts, grappling with data releases and policymaker commentary. Upside from rate relief for valuations may be limited, offsetting but not erasing the effects of elevated valuations. According to Vanguard Australia, Australian equities are expected to return around 4.3–6.3% per year on average over the next decade, and international markets are expected to return 4.9–6.9%.

Although this is lower than returns investors have experienced over the past decade, equities are still expected to play a key role in driving portfolio returns over the long term.

In bond markets, government bond yields have broadly moved sideways as rate expectations recalibrate. While rates may fall in many developed markets, secularly higher neutral rates will likely support bond yields over the longer term. Credit spreads remain relatively tight, but positive supply-demand dynamics, combined with higher yields, may dampen price movements. For aggregate bond indexes, Vanguard Australia expects returns of 3.7– 4.7% for Australian bonds and 3.9–4.9% for global bonds.

Connect with Vanguard™

vanguard.com.au

1300 655 101

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) is the product issuer and the Operator of Vanguard Personal Investor. We have not taken your objectives, financial situation or needs into account when preparing this publication so it may not be applicable to the particular situation you are considering.

You should consider your objectives, financial situation or needs, and the disclosure documents for Vanguard’s financial products before making any investment decision.

Before you make any financial decision, you should seek professional advice from a suitably qualified adviser. A copy of the Target Market Determinations (TMD) for Vanguard’s financial products can be obtained at vanguard.com.au free of charge and include a description of who the financial product is appropriate for. You should refer to the TMD for Vanguard’s financial products before making any investment decisions.

You can access our IDPS Guide, PDSs Prospectus and TMD at vanguard.com.au or by calling 1300 655 101. This publication contains certain ‘forward looking’ statements. Forward looking statements, opinions and estimates provided in this publication are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends,

which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance. This publication was prepared in good faith and we accept no liability for any errors or omissions.

© 2024 Vanguard Investments Australia Ltd. All rights reserved.

QEMUBC_042024_AL