Wealth Architects Quarterly Economic and Market Update

Quarter In Review

Global markets advanced through the first quarter of 2023 with generally positive returns in both equity and bond markets. Inflation and the tightening of central bank policy remained in the spotlight for the markets, punctuated by a spike of volatility triggered by the failing of two large U.S. banks in March, and UBS’s takeover of the failing Credit Suisse in Europe.

The global equity market experienced a strong start in January as markets looked towards signs of fading inflation as a signal that central banks may soon pause the interest rate hiking cycle, providing relief to borrowers. However,

markets reversed course over February as stronger-than-expected inflation data

prompted central banks to continue hiking. In March, the collapse of SVB contributed to a spike in volatility, but the tension was eased as central banks and regulators intervened, soothing market concerns over the banking sector.

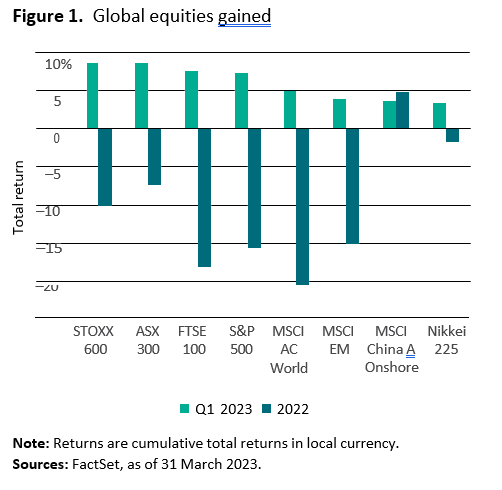

Overall, global equity markets closed the quarter 7.2% higher in local currency terms (Figure 1) as equity indexes held on to their January gains. The S&P/ASX 300 Index returned 3.3% over the quarter as all sectors except energy and financials advanced. Similar sector weakness in global equities were offset by a resurgence in technology companies.

Emerging markets stocks returned 3.8% over the quarter, weaker than their developed peers, as the U.S. dollar strengthened in February,

which can be a headwind for emerging markets equities. Bonds also advanced as investors sought safe-haven assets and expectations for interest rate rises eased (Figure 2).

Economic and market outlook

Since the pandemic, the global economy has recovered strongly, with the demand for goods and services generally outstripping supply. This has helped push inflation to its highest level since the early 1990s and compelled central banks to raise interest rates rapidly in an effort to cool the economy and re-anchor inflation. In Australia, the Reserve Bank of Australia (RBA) has raised interest rates from 0.1% to 3.6% since May 2022, but inflation unfortunately remains well above the RBA’s 2–3% inflation target.

Recent data suggest that inflation has likely peaked, with headline inflation falling from a high of 9.1% to 6.4% in the United States and from 10.6% to 8.6% in the euro area (see Figure 3). Australia’s quarterly inflation data, widely seen as the most reliable gauge for inflation, has also likely peaked. More timely Australian inflation-related measures suggest that inflation is now on a downward path.

Figure 3. Inflation has peaked in most developed markets

With inflation pressures easing, we expect central banks, including the RBA, the U.S. Federal Reserve and the European Central Bank, to soon pause the interest rate hiking cycle (see Figure 4). A pause allows central banks time to assess the impact of higher interest rates, which typically take one to two years to fully pass through to economic growth and inflation. However, the key risk is that inflation remains stubbornly high and central banks are forced to resume the hiking cycle.

Markets have remained focused on inflation and central bank policy year to date, driving volatility in equity and bond markets alike. Clear signs have now emerged that inflation has peaked, and as such markets are now pricing in a slowing pace of interest rate hikes. This has resulted in falling yields that have benefited bond prices quarter-to-date but are expected to moderately reduce forward-looking returns.

Despite recent declines, yields and fixed income valuations continue to be more attractive than they were a year ago when interest rates sat close to historic lows.

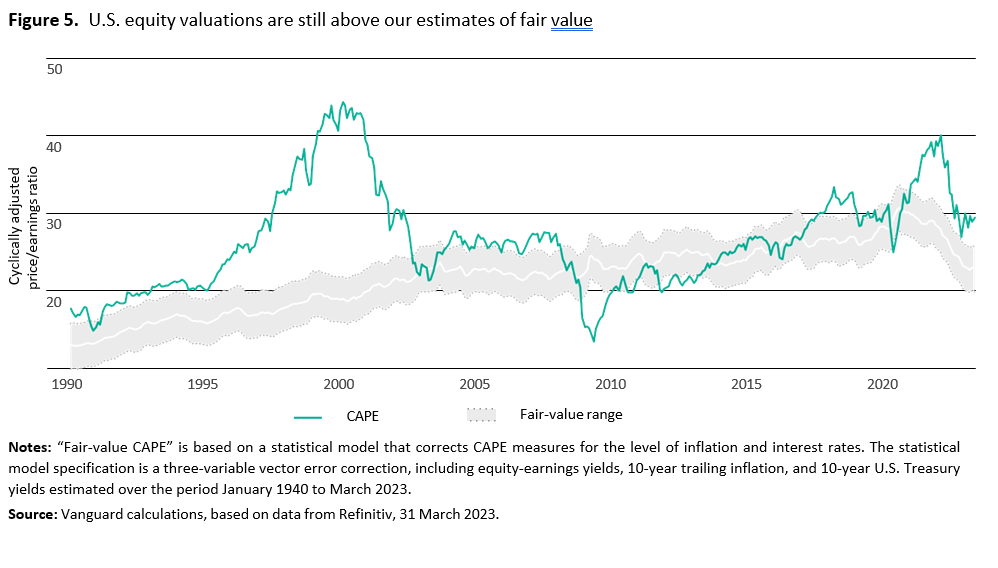

Meanwhile, equity valuations have remained relatively robust year-to-date despite a guarded view on corporate earnings. Figure 5 shows a long-term measure of

U.S. equity valuations, the cyclically adjusted price-earnings (CAPE) ratio, against Vanguard’s estimates of fair value. Although cheaper markets are more fairly priced than a year ago, valuations are still sitting above their fair value when adjusting for current levels of interest rates and inflation. This presents potential downside risks for equities particularly if inflation remains stickier or if earnings expectations disappoint.

As volatility persists it’s as important as ever for investors to remember their investment plans. For most investors, ensuring their plans continue to align with their investment goals, staying diversified, and maintaining discipline, are all well worth a reminder.